The Trump administration took office in the United States in January 2025. As early as January, tariff reinforcements on aluminum and steel were announced, and on March 26, tariff rates determined for each country worldwide were announced. Japan was set at 25%, which would be imposed on a wide range of Japanese export industries including automobiles. Here, we will organize the impact on the automotive industry over the past six months regarding the Trump tariffs, which are said to transform global trade and the economy. (Note: Japan's exports to the US already had a 2.5% tariff imposed, and with the additional 25% imposed, the automotive export tariff to the US became 27.5%).

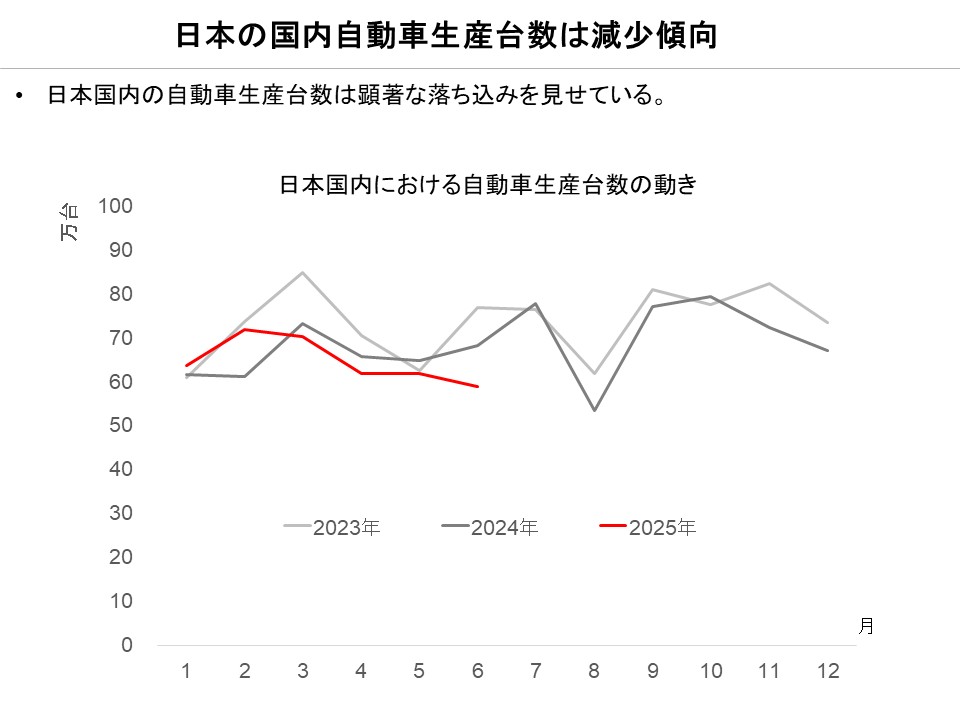

Automobile production in Japan is clearly showing a declining trend

The graph at the beginning shows a monthly comparison of automobile production and sales volumes for China and Japan respectively. Looking at this, domestic automobile production in Japan has clearly decreased since the beginning of this year. Japan's domestic automobile production still has a high dependency on exports to the US, with 10-20% or more of total production being exported to the US. Depending on the manufacturer, some still have high dependency on the US market, with over 70% going to the US (Mazda) and half going to the US (Subaru). In contrast, China's automotive industry was a latecomer and has not been able to expand overseas, but has fully benefited from its massive domestic automotive industry, increasing both production and sales volumes. (However, China's statistics count automobile sales on a factory shipment basis, and there is a possibility that vehicles are actually being shipped but not selling = excess inventory is accumulating, which requires attention going forward.)

The 25% + existing 2.5% tariff (total 27.5%) on automobile exports from Japan to the US was actually imposed and collection began in the US in March of this year. However, domestic production volumes can be seen to have already started declining in February, anticipating the tariff implementation. Production levels thereafter have continued at levels below last year and the year before. In July, through tariff negotiations, the US basic tariff rate against Japan was agreed at 15%, but this was not immediately implemented, and the 27.5% tariff rate continued for several months. In September, a written agreement was finally reached, and the automotive export tariff is about to be implemented at 15%. The confusion surrounding tariffs has reached a tentative settlement. This can be said to have reduced uncertainty. However, considering that a 15% tariff will probably occur permanently going forward, it can be said that there is a high possibility of gradually serious impact on Japan's domestic automobile manufacturing.

Trump tariffs may possibly achieve a certain level of success.

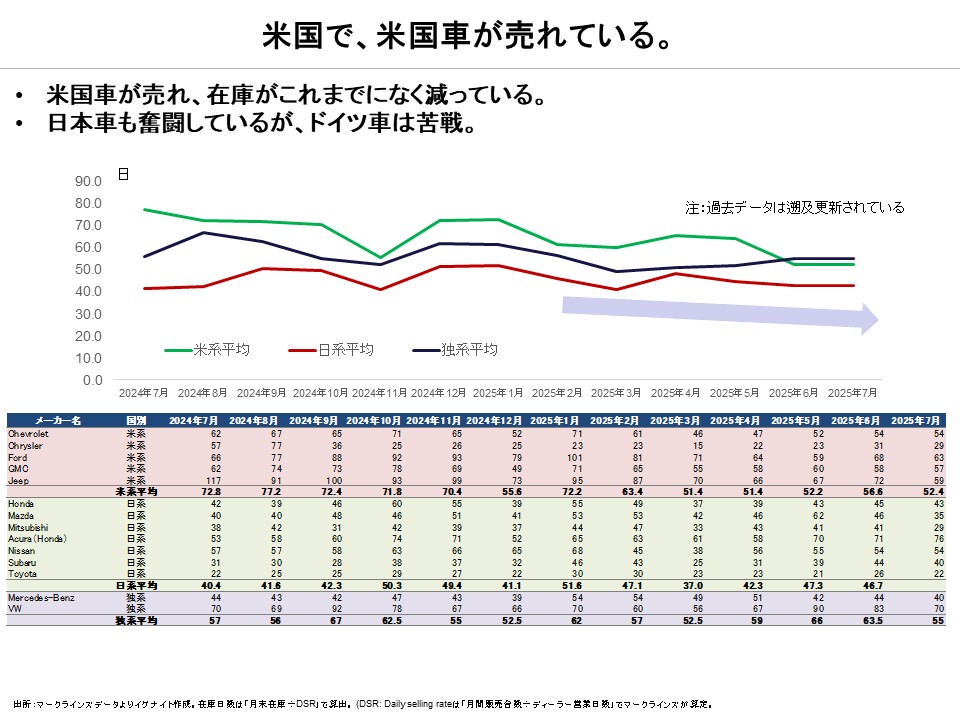

The sign indicating this is the inventory situation of automobile manufacturers operating in the US. (Chart above) This graphs the average inventory days by grouping the inventory days of automobile manufacturers selling cars in the US into "US groups," "Japanese groups," and "German groups." Looking at this, it can be seen that US manufacturers' inventories have decreased significantly. It is empirically known that US manufacturers hold considerably more inventory compared to Japanese manufacturers. This is because supply chains that minimize inventory, such as just-in-time production, are not as strong as those of Japanese manufacturers. However, a bigger factor is that US users dislike "stockouts." They want to come to the dealership, see the actual car, and be able to drive it immediately. Even if they can't drive it home on the spot, it's important that they can drive it within at most a few days to a few weeks. For this reason, US manufacturers' average inventory days are generally around 60 days on average. However, since the beginning of this year, US manufacturers' inventory levels have visibly decreased. This decrease is more pronounced compared to Japanese and German manufacturers. While tariffs have been implemented on Japanese and German manufacturers selling in the US, US manufacturers are naturally not directly affected by tariffs (though there are effects such as price increases for imported parts).

The purpose of Trump tariffs is the "revival of US manufacturing." Whether tariffs can truly achieve this remains to be seen. While negative opinions predominate, if this inventory decrease (strong sales) of US manufacturers means the "revival of US automobile manufacturers," Trump tariffs might possibly achieve certain results contrary to most expectations. However, it is still too early to draw conclusions, and it will be necessary to closely monitor future inventory levels and sales trends.

Meanwhile, Japanese manufacturers have not significantly increased their sales inventory even after tariff introduction, and sales volumes in the US have not dropped significantly either. Tremendous rationalization efforts, management efforts, and US customers' trust in Japanese cars are currently preventing a drop in sales. In contrast, German manufacturers' sales inventory has decreased notably, suggesting the struggles of German manufacturers in the US market.

A major wave of transformation is once again arriving in the automotive industry

Actually, major transformation in the automotive industry is not limited to this alone. In the electric vehicle market, which was once excessively heated and then corrected, various changes and signs of new risk materialization are gradually appearing. Next time, we will analyze the changes creeping into the global electrification market.